Beginner investor guide

How to Underwrite Your First Rental Using DealPrism

A simple, beginner-friendly walkthrough for checking rent, expenses, financing, and downside risk before you buy your first investment property.

Start here

Underwriting your first rental in DealPrism means putting rent, expenses, financing, and reserves into one deterministic model so you can see whether the deal still works after realistic assumptions are applied.

The beginner advantage is not complexity. It is consistency: use the same framework every time, pressure-test the downside, and avoid letting excitement fill in missing numbers.

What underwriting actually means

Underwriting a rental means estimating how a property may perform before you buy it. In practice, you are pressure-testing one question: does this property still make sense after you use realistic assumptions?

For a beginner investor, that matters more than building a complicated spreadsheet. You do not need a perfect model. You need a consistent way to estimate rent, account for expenses, include financing, and see whether the deal still works when the assumptions get less friendly.

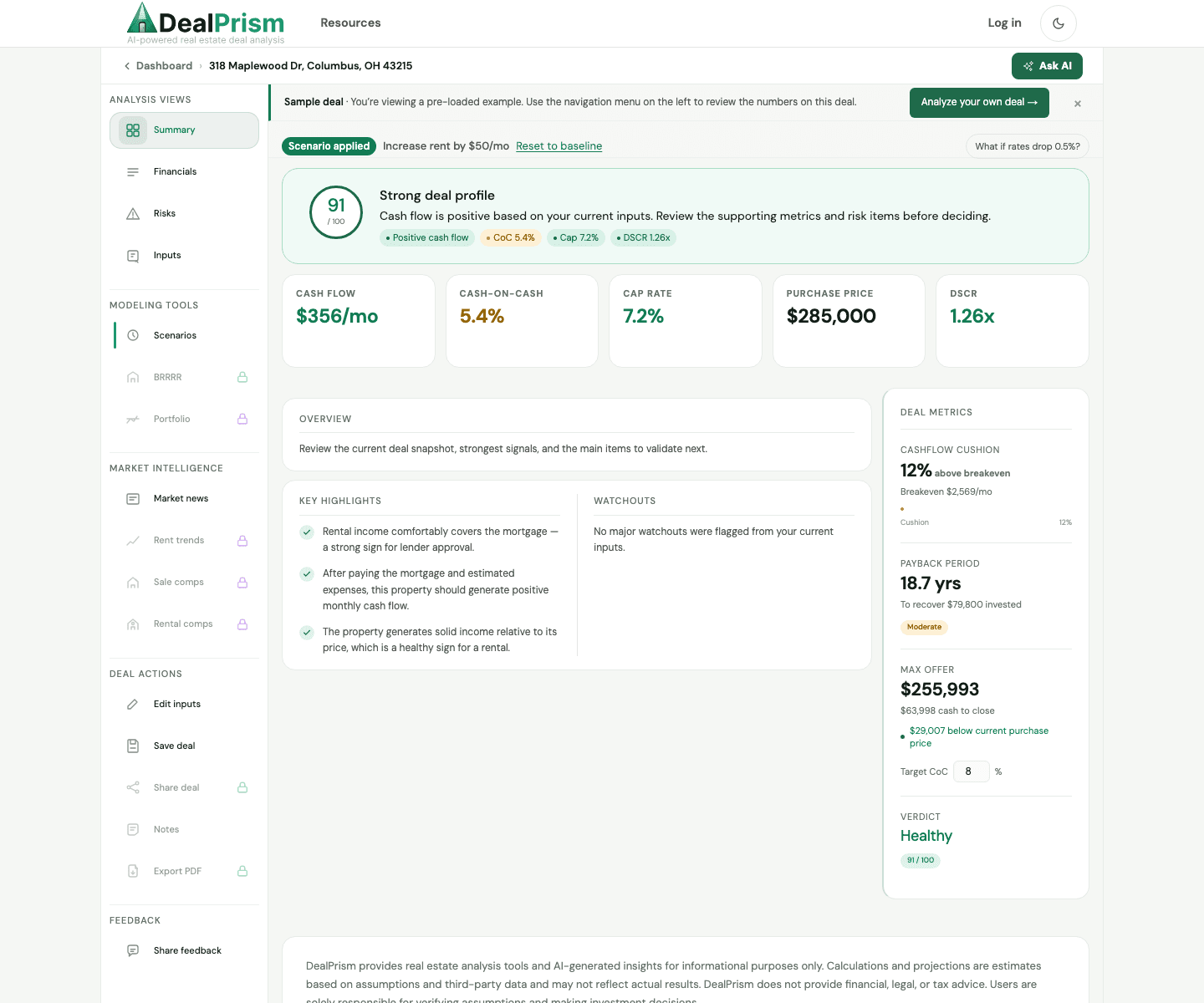

DealPrism helps by organizing the inputs and surfacing the outputs most investors care about first: cash flow, cap rate, cash-on-cash return, DSCR, and the assumptions behind each number.

A simple underwriting checklist

| Stage | What to enter or verify | What can go wrong if skipped |

|---|---|---|

| Purchase and financing | Price, down payment, rate, term, closing cash, rehab budget | The monthly debt load and cash to close get understated |

| Income assumptions | Rent supported by real comps, not best-case listing optimism | The whole deal can look healthier than it is |

| Operating expenses | Recurring costs like taxes, insurance, management, HOA, and utilities, plus set-asides for vacancy, maintenance, and CapEx | Missing expenses create fake cash flow |

| Stress testing | Lower rent, higher vacancy, more repairs, or worse financing | A fragile deal can look safe in a single base case |

The four numbers to focus on first

Cash flow

Monthly

How much cash may remain after expenses and debt service

Cap rate

Property-level

Yield before financing enters the picture

Cash-on-cash

Investor-level

Return on the cash you actually put into the deal

DSCR

Debt coverage

How comfortably NOI may cover the mortgage

Those metrics do different jobs. Cash flow tells you whether the deal may put money in your pocket each month. Cap rate helps you compare properties independent of financing. Cash-on-cash return shows whether your upfront cash is working hard enough. DSCR helps you understand debt safety and lender sensitivity.

Example DealPrism screens

The screenshots below are captured from DealPrism's actual sample analysis workspace. They show the real flow from reading the metrics to pressure-testing the assumptions and asking grounded follow-up questions.

Step 1 — Start with purchase price and financing

Before you worry about advanced metrics, enter the numbers that define the structure of the deal:

- Purchase price

- Down payment

- Interest rate

- Loan term

- Closing costs

- Any upfront rehab budget

These numbers shape both your cash needed to close and your monthly debt payment. A property may look affordable from the listing price alone, but the actual cash required can be much higher once you include closing costs and repairs.

Step 2 — Use realistic rent, not best-case rent

Most first-time investors do not lose deals because they forgot a formula. They lose deals because they used optimistic rent.

When you underwrite in DealPrism, use a rent estimate you can defend with comparable rentals. If the range appears to be $1,550 to $1,700, underwriting at $1,850 just to make the math work is not conservative analysis.

If you are unsure, a good beginner rule is simple: round rent down and round expenses up.

Step 3 — Include the expenses beginners usually miss

Good underwriting is usually less about adding clever formulas and more about refusing to ignore real costs.

The easiest way to stay clear is to separate true monthly costs from reserve-style allowances. Taxes, insurance, management, HOA dues, and utilities are regular bills. Vacancy, maintenance, and CapEx are amounts you set aside because the pain shows up intermittently, not because a bill arrives on the first of every month.

- Property taxes — a recurring property cost that should be verified with local records.

- Insurance — a recurring cost; use landlord insurance, not a homeowner assumption.

- Property management — a recurring operating cost worth modeling even if you plan to self-manage today.

- Vacancy — a set-aside for lost rent during turnover or nonpayment.

- Maintenance — a reserve-style allowance for routine repairs and upkeep.

- CapEx reserves — money set aside for roofs, HVAC, water heaters, and other larger future replacements.

- HOA or utilities where applicable

DealPrism's analysis flow is designed around these assumptions because a rental that only works after several expenses are ignored is usually not a strong beginner deal.

Step 4 — Understand the core underwriting math

Where:

- Monthly NOI

- Effective gross income minus recurring operating costs and reserve-style allowances, before the mortgage

- Monthly Debt Service

- Principal and interest, plus any additional debt-related payment obligations modeled in the deal

Example:

- Estimated monthly rent = $1,850

- Vacancy at 8% = $148

- Effective gross income = $1,702

- Operating expenses = $702

- Monthly NOI = $1,000

- Monthly debt service = $842

- Monthly cash flow = $158

Based on the current assumptions, this deal may generate positive monthly cash flow. But a beginner should still test what happens if rent softens or expenses rise.

Step 5 — Check the deal from more than one angle

A first rental should not be judged by cash flow alone. DealPrism helps you view the same property through several lenses:

- Cash flow — monthly income potential after expenses and debt

- Cap rate — property yield before financing

- Cash-on-cash return — return on the cash you have tied up in the deal

- DSCR — whether NOI appears to cover the mortgage with enough buffer

If one number looks strong but the others look weak, pause and figure out why. A deal with decent cap rate but weak cash flow may have financing pressure. A deal with positive cash flow but poor cash-on-cash return may require too much cash up front.

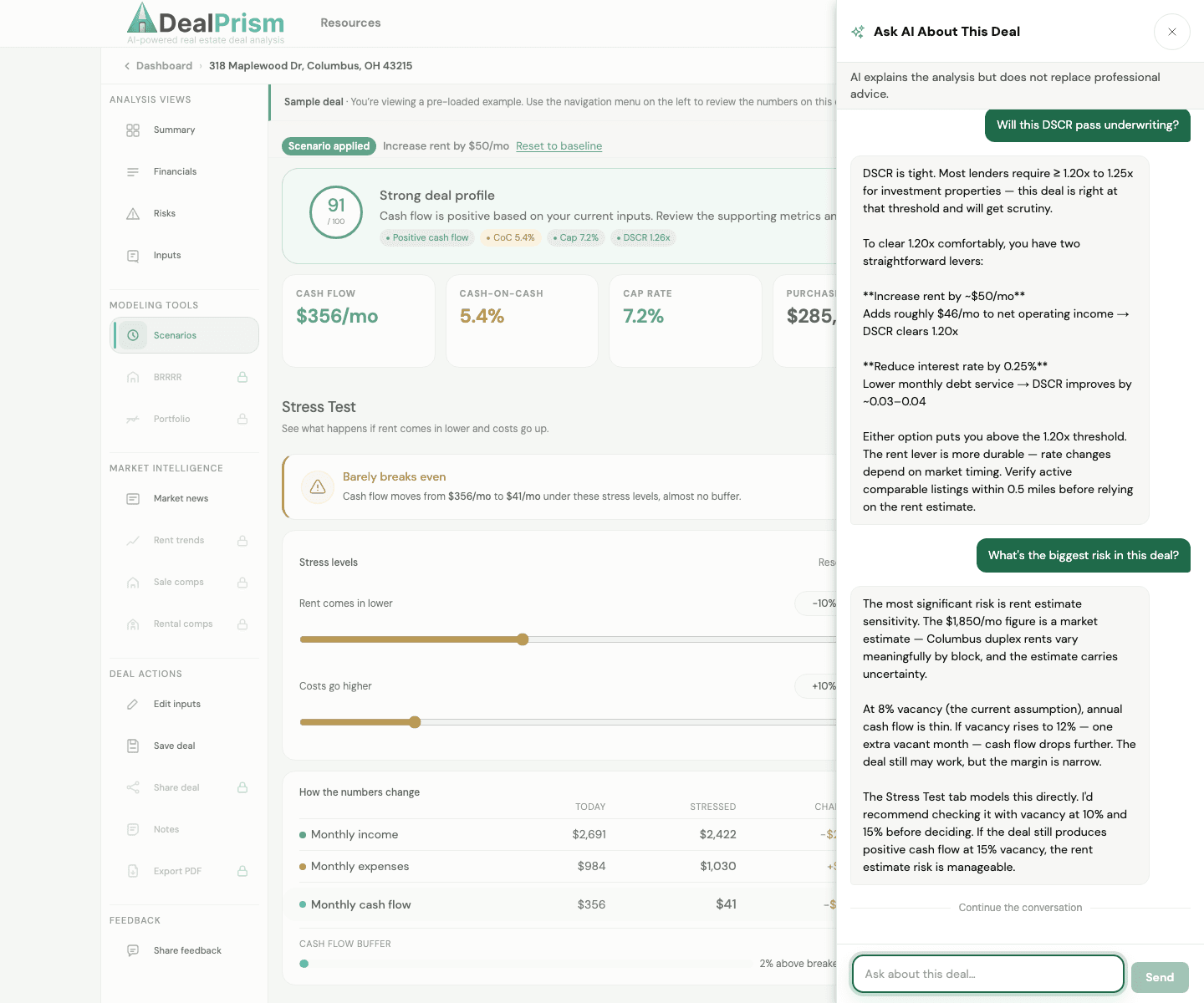

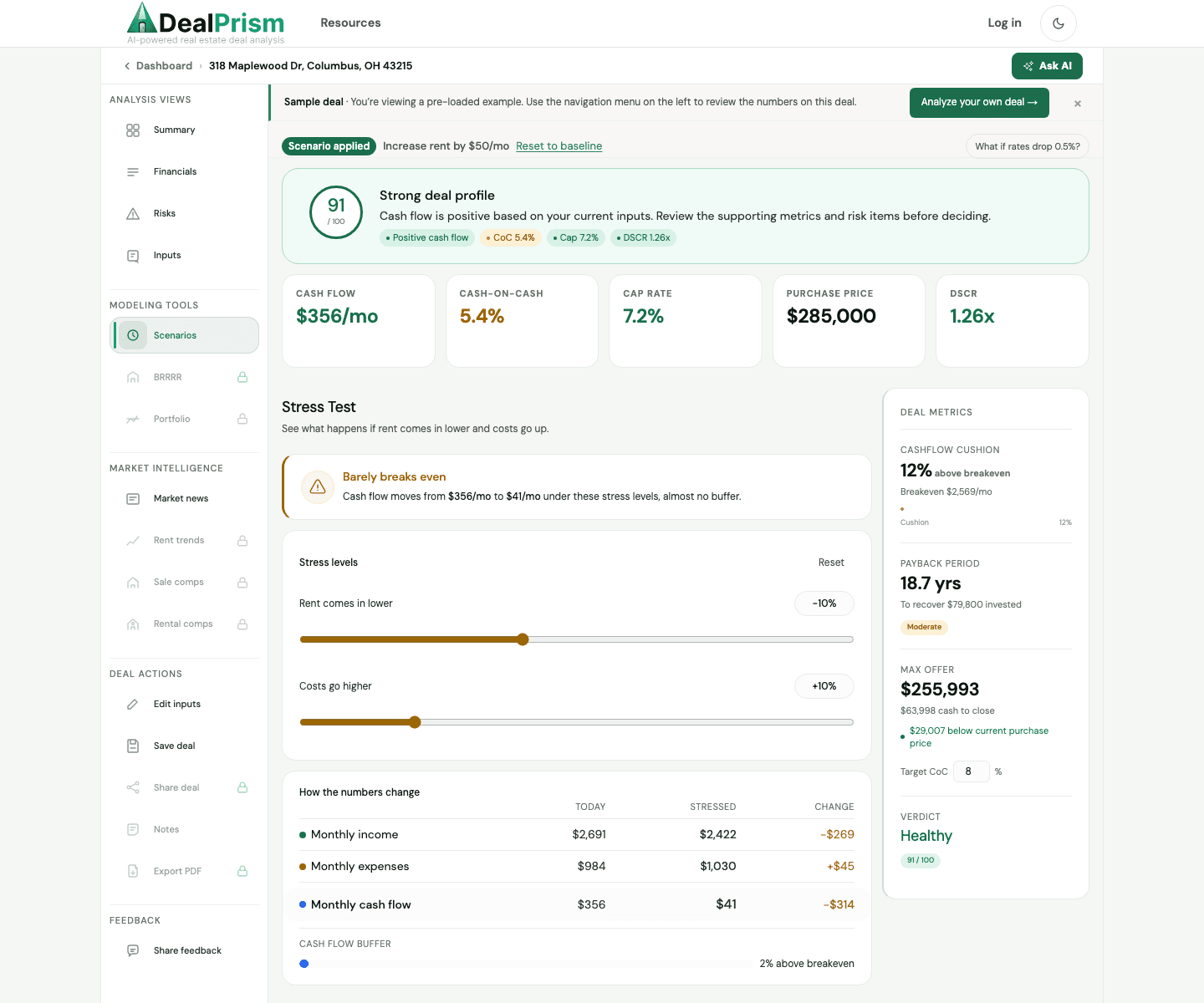

Step 6 — Stress-test before you trust the deal

This is one of the most useful parts of underwriting your first rental in DealPrism.

Once the baseline numbers are entered, test a few less-friendly cases:

- rent comes in lower than expected

- vacancy is a little higher

- maintenance or insurance costs rise

- the property needs professional management later

If the deal collapses as soon as one assumption moves against you, that may be telling you the margin of safety is too thin.

Step 7 — Decide with criteria, not excitement

By the end of the analysis, try to put the property into one of three buckets:

- Yes — the deal appears to work under realistic assumptions

- Maybe — the deal may work at a better price or with better financing

- No — the assumptions do not leave enough room for error

That discipline matters. Beginners often start with a property they want to buy and then try to force the math to support it. A better process is to let the assumptions and outputs narrow the decision for you.

What DealPrism is actually helping you do

DealPrism is not replacing due diligence, lender quotes, inspections, or local market research. What it can do is make your first-pass underwriting more structured and easier to question.

That matters because most beginner mistakes are not about failing to memorize formulas. They come from skipping expenses, using hopeful rent, or trusting a deal before testing the downside.

If you want a broader foundation first, read How to Analyze a Rental Property. If you want to separate yield from financing effects, continue with Cap Rate vs Cash Flow and Cash-on-Cash Return Explained.

Frequently asked questions

- What does it mean to underwrite a rental property?

- Underwriting a rental means estimating how a property may perform before you buy it. That includes purchase price, rent, recurring operating costs like taxes and insurance, reserve-style allowances like vacancy and CapEx, financing, and the return metrics that help you compare one deal to another.

- What numbers should a beginner check first?

- Start with monthly rent, mortgage payment, and the main operating expense buckets. Split those buckets into recurring costs like taxes, insurance, and management, and reserve-style allowances like vacancy, maintenance, and CapEx. Then look at monthly cash flow, cap rate, cash-on-cash return, and DSCR to understand income, yield, capital efficiency, and debt coverage.

- Can DealPrism tell me whether I should buy a rental property?

- No. DealPrism helps you analyze the assumptions and estimated outputs, but it does not make the decision for you. Results depend on the rent, expenses, financing terms, and property condition you use.

- Why should I include property management if I plan to self-manage?

- Including management gives you a more conservative view of the deal. It helps you understand whether the property still works if you eventually outsource management or if your time becomes more limited.

- What if the deal only works with optimistic assumptions?

- That is usually a warning sign. If a rental only works when rent is high, vacancy is low, and expenses stay unusually light, the margin of safety may be too thin for a beginner investor.

Related resources

Run your own first-rental analysis

Enter a property, review the assumptions, and see estimated cash flow, cap rate, cash-on-cash return, and DSCR in one place. Results may vary if rent, vacancy, expenses, or financing differ from the assumptions used.

Analyze your own dealResults are based on user-entered assumptions. Values may vary by property, location, and market conditions. Review all assumptions before making investment decisions.